Solving the Buy-in Paradox

Here’s the buy-in paradox facing private companies. Top talent drives company growth and value. Higher company value dissuades top talent from buying into an illiquid company. Frustrated talent leaves and company value falls.

Public companies benefiting from daily valuation and immediate liquidity can readily solve this buy-in puzzle with stock options and restricted stock. Private companies are not so lucky.

Success Creates its Own Challenges

In the early stages of a start-up, buy-in capital may be cheap, perhaps $10,000 for 10%. Grow to $10M in value and now 10% is $1M, beyond the comfort zone for the typical executive. Grow to $50M in value and at $5M, buying a 10% ownership stake becomes nearly impossible for an individual. Clearly, success creates its own challenges.

Typically there is no single solution to solve this buy-in paradox. Solutions differ for newly promoted executive owners coming into the ownership suite versus a proven CEO who deserves greater percentage of ownership.

Trio of Solutions

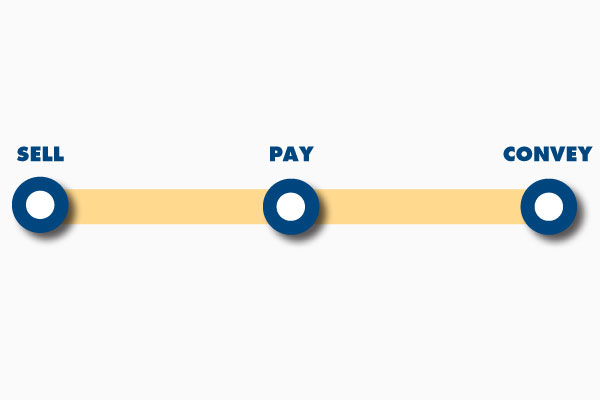

Here’s the buy-in challenge: how do we simultaneously increase shareholder value while making the buy-in more affordable for critical executives? We call the portfolio of solutions to address the buy-in paradox SELL • PAY • CONVEY®. Notionally, we can make it easier for key executives “get-in” to the ownership suite in three major ways:

- SELL: The company (or the existing owners) SELLS executives equity with attractive terms to mitigate risk.

- PAY: The company PAYS executives with equity – typically called a compensatory grant.

- CONVEY: The company CONVEYS ownership to executives with no buy-in or compensatory cost.

Here is a single example from each of the SELL • PAY • CONVEY® strategies:

- Sell equity using a mix of recourse and non-recourse debt to mitigate buy-in risk.

- Most equity buy-ins involve installment notes. If the executive buyer defaults on the note, the non-recourse portion of the note is satisfied with the return of the shares. Borrow $1M at 50% recourse and 50% non-recourse, and the maximum cost in event of default is $500,000. Be careful here. Many tax practitioners advise that equity purchases with more than 50% non-recourse note can trigger stock option treatment (ordinary income tax rate), rather than the desired capital gains treatment.

- Pay equity on a favorable basis reflecting minority interest discount.

- The use of minority interest discounts in a buy-sell agreement is not required, yet often advisable. Grant an executive 10% of your $10M company and how much tax on compensation is due? If no discounts for lack of marketability and lack of control, compensation is $1M. After a 40% discounts, the compensatory income is much less at $600,000. Apply a 40% income tax rate and the tax due before and after discounts are dramatically different: $400,000 vs $240,000.

- Convey equity via profits interests in a partnership or a qualifying LLC.

- Provide profits interest which is a unique type of ownership with no cost at transfer. A grant of profits interests provides an executive all the upside of a grant without the need to pay the underlying “threshold” value. Further, qualifying a profits interest grant conveys property rights and is taxed at capital gains rates.

Overcoming the Core Challenge of Succession Planning

Just about every business owner must ask and answer the key strategic question: how do we efficiently and effectively provide some “taste of ownership” to our top talent? Mastering strategies of Sell, Pay and Convey helps address this critical succession planning challenge.

How many of the “Sell • Pay • Convey®” strategies has your ownership team explored?

Please contact us to learn more.